Background

An Opportunity to Impact Millions

India is a country of roughly 140 crore people, yet only about 3 crore invest in the market, making up a mere 2% participation. In comparison, about 56% people invest individually in the US.

While the Association of Mutual Funds in India have done a great job of promoting investments with the 'Mutual Fund Sahi hai' campaigns, the biggest problem in participation comes in the immediate next step, 'Kaunsa fund sahi hai?' (Which fund is right?).

There are hundreds of funds spread across various market caps, operating in active and passive formats, taking a direct or regular

distribution route. Each with complex terms like NAV, XIRR, Expense Ratio, Exit Load etc. Which confuses and intimidates people, combined with a low trust environment.

This is exactly what Paddy (2x founder, SaaS), Jags (SaaS Founder, Mentor CISCO launchpad), and Vikas (Investment Expert, Ex-IIM, Goldman Sachs) saw as an opportunity and set out to solve.

The idea was simple, build a goal-based investment advisory platform and make it rewarding.

My Role

Founding Product Designer

I joined an early team of 10, including the co-founders, backend team, and product architect, to embark on a project aligned with relatable problems within my own investment journey. On top of this, the chance to think about gamification in finance made it doubly exciting.

My responsibilities included:

-

Defining features and functions to envision a product

-

Developing a product and gamification strategy

-

Establishing UX foundations and processes

-

Designing the UI and creating a design system

-

Collaborating with the front-end team to test & implement

-

And the initial marketing collaterals

Outcome

We built the beta of the World's 1st Invest to Spend platform within 6 months and became its first user in Diwali 2020. Over the next 3 months, we tested and launched the product & onboarded hundreds of people organically.

We also set processes to align product, marketing and business functions, defined our KPIs and started marketing campaigns, leading to more users, reviews and investments.

9,218.2

Average Monthly Active Users between Jan 2021 to Dec 2021

66.07%

Profile Completion Rate (Filling bank details and creating mandate) within 1 week of Sign up

180 K+

Downloads from Play Store and App Store between Jan 2021 to Dec 2021

Design Philosophy

Radical innovation through deep understanding of existing problems, with a focus to create a distinct market advantage

We wanted to experiment, iterate and ship ideas fast. It required the team to be aligned towards the core vision and have similar expectations from the outcome, the product needed to be relatable for customers - be a no-brainer in its value proposition and not just another investment tool.

Approach

I made a structure that focuses on 3 fundamental aspects of building the product - the business, the users and the market

1. The Business: Core vision and alignment

Understanding value proposition and ideas including the Investment advisory model, the revenue model, the marketing strategy, and the expected product adoption rate to make a meaningful cohesion

2. The Market: Solutions and opportunities

Research existing platforms to understand what is working, what is trending, what is not working and objectively inspire features and functions including tech.

3. The Users: Understand and solve the user journey

Finding the needs and motivations of users at each stage of the journey, deriving solutions and seamlessly connecting the whole

The Business

I focused on understanding the vision of key stakeholders, the problems they aimed to solve, and their initial ideas. I also set agreement on outcomes, deliverables, and timelines to guide the project.

1. Process and Timeline

I created a timeline and structured process to kickstart the project. Using a slightly adapted double-diamond approach, I allocated more time to the exploration and broadening phases than to narrowing down.

Dedicated slots were set aside for development support, along with regular stakeholder meetings to maintain alignment and foster collaboration.

I collaborated with key stakeholders, including the co-founders, product architect, and head of marketing, to understand the company’s vision, target audience, and product positioning goals.

2. Company's Vision

I compiled the insights into a Vision Board, outlined desired features, and developed a product adoption strategy to focus on strategically significant customers.

Vision: Empower every Indian to get the best value on their expenses with goal-based financial decisions. At Multipl, we simplify investing with expert advisory and gamification, allowing people to save, invest, and earn rewards for spending on life’s milestones—big or small.

3. Working of the Investment Advisory

Multipl Wealth Management is a SEBI-registered investment advisor, which means it can offer recommendations to individuals. RIA Services are often expensive and it needs a larger capital to be managed.

The idea was to solve this and make personalized wealth management affordable and accessible to more people.

Low ticket size makes advice affordable

Personalized mutual fund recommendations started at just ₹1000, lowering the entry barrier for everyday investors.

S-L-R philosophy ensures smart portfolio

Recommendations prioritises Safety of capital, Liquidity and High Retunrs for each goals, risk profiles, & financial situations.

Direct funds reduced unnecessary costs

Eliminated broker distribution charges by recommending only direct mutual funds, making the service more cost effective

Transparency to build user trust

Provided clear insights into fund details, their workings, and the expertise managing investments, fostering confidence.

4. Gamification & Other Key Aspects

Gamification was imagined as an integral part of the UX, a system to function both as a reward for users and as a revenue model through brand partnerships.

Other essential processes such as KYC, Bank Mandate, FATCA details were prioritised first to help the development team make progress, as these have straightforword solutions with good precedence.

Rewards to celebrate progress and drive actions

The system was designed to acknowledge user progress, prompt subsequent actions, and offer relevant choices in rewards.

Simplified profile completion and tracking

Progress and time estimates for completing profile sections, helping users stay informed about each steps.

Balanced economy for steady motivation

The system's economy was balanced to maintain progress and motivation, encouraging users to engage more with the app.

Develop trust by showing how the system works

Informing in details about allocation for various risk profiles, fostering understanding of personalized strategies.

The Market

I analysed hundreds of reviews from Playstore and Appstore along with comments, discussions and marketing materials on social media for popular broking, banking services and gamified solutions to find broader themes and insights on the topic of personal finance and gamification

Research Method and Observations

Read and categorised user comments in store by themes and ratings for apps like Paytm Money, Groww, Scripbox. I also went rhrough their social media pages to get a broader idea about what ticks with the users.

I looked at examples of gamification in financal services and tried to understand the system with a focus on the strenghts and weak ness of the system

Insights from Investment Products

Keep it simple and clearly present facts

Users appreciated the simple and clean design of apps like Groww and Qapital. Tools like SIP calculators and financial summaries were valued for their practicality and ease of use, transparency in charges was paramount for coming back.

People will give personal info. when they see the value

Many apps collect users' information during onboarding with an extremely high success rate. The online KYC processes in apps like Paytm Money were highly appreciated for their convenience, reducing the friction in starting to use the app.

Break the mechanical expereince

Many users felt that existing saving products lacked a rewarding experience. The process felt mechanical, and there was little incentive to continue using the app beyond an investment tool.

Provide options for customisation

People wanted options such as pausing investments, changing bank account, ability to choose custom duration for SIP instead of only the monthly option.

Insights on Gamification

Intrisic rewards can be long term motivators

Although extrinsic rewards bring large no. of customers, the design should try to induce intrinsic rewards such as sense of achievement, personal growth, learning and enjoying the task.

Simulations are great tools for learning

Simulators are best used to educate people in time taking and high risk scenarios. This should not be forced within the core experience, it should try to validate users decisions.

Elements of rewards should have a meaningful cohesion

Types of rewards, Time of rewarding, Amount of reward, Interaction to get rewarded. The combination of this should feel meaningful and desirable (more is better and slightly challenging)

Challenges can be powerful guide for progress

Personalised challenges, clear progression paths within the product, coupled with relevant feedbacks regarding users actions can be very powerful in guiding users towards an outcome

The User

I conducted primary user research to understand the needs and pain points of investors, for this i categorized them into newcomers and existing mid-long term investors. To understand goals relevant for users, I did a secondary research through a social media survey.

Customer Segmentation

Initially, the team considered catering to everyone, which risked developing an unfocused solution. After a short qualitative research, we found that salaried people above 45 years viewed the stock market as too risky and preferred tangible assets like real estate and gold. They only trusted people who were directly accessible for financial advice.

On the other hand, people below 27 found it hard to prioritize investing, preferring to spend on lifestyle needs. However, those aged 27-40 actively sought investment solutions and were willing to trust new platforms. This was the sweet-spot and this group became our primary audience, with others as secondary.

Research Method & Personas

The aim of this research was to understand the first hand behavior of the target segements, in context to their spending, saving and investment preferences.

We considered the following specifications; Tier 1 city dwelling individuals, between the age of 25-40 years.

Also, recording their monthly income, amount/percent of income saved, spent and invested, tools or modes of investment.

Methodology :

1. Filtered Ideal candidates through a survey questionnaire.

2. Telephonic/Video Call based one-on-one interview.

Why to Invest?

Identified Problem

We discovered that wealth creation was the main reason people wanted to invest, but many didn't prioritize to actually do it. This posed a significant challenge, as despite understanding the benefits, they delayed investing.

Reason for this was that people often struggled to predict how present actions will impact their future, leading to procrastination in investment decisions. This tendency to avoid immediate efforts for future gains made it difficult for them to see wealth creation as a priority.

Proposed Solution

Our solution was to help people visualize specific and relatable outcomes and instantly take the first step. Inspired by positive visualization, a popular technique in psychological literature, we came up with 'Goals' to nudge imagination in various lifestyle categories like travel, gadgets, and long-term needs such as buying a home or retirement.

This approach made aspirations tangible and helped users discover new goals they hadn't considered before, such as hobbies and gifting. By making future achievements more concrete and relatable, we were able to seed a strong 'Why'.

How Much to Invest?

Identified Problem

People generally understood the need to invest 20-30 percent of their income, a notion popularized by finance influencers on social media. However, this advice often overlooked the timing of investments towards specific outcomes, creating a false sense of perpetual growth.

When financial emergencies arose and markets were down, investors faced losses, leaving them disappointed about not being able to use their money beneficially. This mismatch between withdrawal timing and fulfilment of goals - highlighted the difficulty in associating investments to financial goals.

We found that for similar goals, people attributed amounts that were within a comparable range irrespective of age or income.

Proposed Solution

We created goals driven by amount and time, designing a system to show approximate returns based on the target amount and date. The returns adds up with investment to fulfil the target amount, allowing users to always invest less than the target and even lesser with a longer target date.

We made amount recommendations for each goal based on popular market value of goals in similar categories to give people an anchor point for reference.

The system enabled users to choose and customize their goals, making the process more personal. This approach leveraged the popular IKEA effect, where users value the solutions they have helped create.

Where to Invest?

Identified Problem

People often started investing in sectors they were familiar with, such as IT, Automobile, and Power, but lacked knowledge about market caps and industry dynamics. They were unsure how much to invest in large cap or mid cap for different time periods or if small cap was suitable for short-term goals.

People are introduced to these investment solutions by banks and brokers, and most of them are placed into regular and active schemes with brokerage and maintenance charges, leading to higher costs. This lack of clarity and guidance on where to invest often resulted in suboptimal investment decisions and unnecessary expenses.

Proposed Solution

Our investment advisory provided a comprehensive solution by focusing on two broad parameters: the user profile and the filtering system. We assessed risk tolerance, investing experience, income, expenses, and more, categorizing users into four groups: conservative, moderate, growth, and aggressive. The Safety-Liquidity-Return philosophy then filtered 2-5 funds from over 1500 direct funds based on the goal's time and amount.

Inspired by popular broking apps like Groww and Zerodha, we designed the profile input to be user-friendly. We added elements like risk profile, asset allocation, and our investment philosophy to inform users and build trust.

How to Stay Motivated?

Identified Problem

Staying invested proved to be a major challenge for successful investing. Our research identified two key issues: lack of time in planning and difficulty in organizing outcomes that correspond well to anticipated life events.

People often felt investing required active involvement and significant time to monitor progress, analyze portfolios, and make changes. Additionally, many invested without specific outcomes in mind. In emergencies and to fulfil ad hoc goals, they spent more than anticipated, depleting their funds and delaying other goals, leading to regret and a lack of motivation to stay invested.

Proposed Solution

We automated payments with a bank mandate and rebalanced portfolios with user consent, addressing the lack of time. The 'Journey' section tracked progress of each goal and informed users about their overall investments, giving a sense of proportion about their contributions. This application of the Goal Gradient Effect helped users feel closer to their targets, boosting motivation. A simple withdrawal process allowed users to experiment and develop trust.

Additionally we designed a reward system with an in-app currency called 'Mbits' - awarded for progress in goals. Users could redeem Mbits to avail coupons from a list of brands.

Testing & Optimisation

-

Removed Challenges to Promote Self-Exploration:

The challenges feature worked in guiding users for the next steps, but users relied too heavily on it to progress further. It discouraged self-exploration which was crucial for long-term engagement, therefore we removed it.

-

Introduced Coach-marks & FAQs to aid in getting started:

Users needed guidance to get started, understand how things work, set up the profile and start their first goal, we introduced coach marks and FAQs to help with this.

-

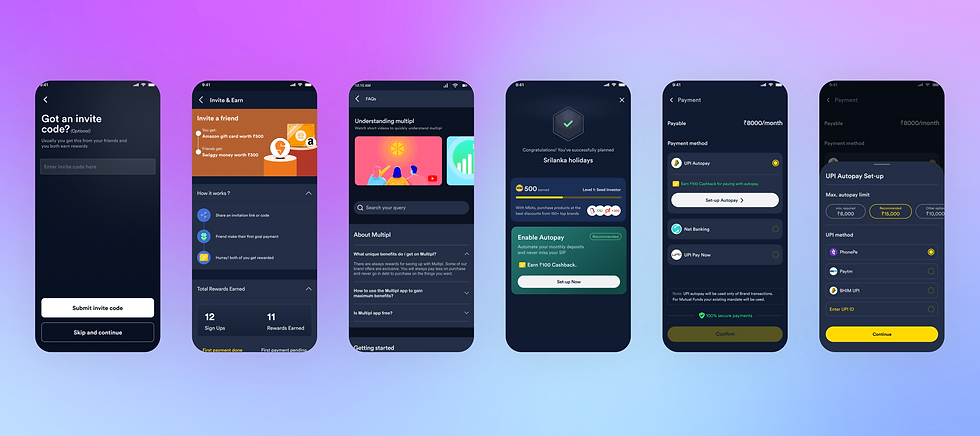

Added Referral System to Promote Organic Sharing:

We missed considering making a sharing ecosystem until the beta release, this became an immediate priority which we solved through a referral system and launched within the next 3 months. Users get incentives for inviting their friends into the app and when their friends create their first goal, nudging users to be promoters of the app.

-

Sachetized Bank Mandates With UPI Autopay:

We solved for trust barriers that required users to create bank mandate of larger amounts that enables recurring payments for goals they have created, we did it by introducing UPI autopays of smaller amounts - enabling them to put only the amount required for goals.

Conclusion

'Save Now-Buy Later' was coined to embody the unique Goal-based Investment Advisory model as an alternative to the then popular debt-driven 'Buy Now-Pay Later' philosophy. Multipl, since has been recognized as one of the most innovative financial products and praised for its user-friendly design. The model later evolved to include features such as brand offers linking savings to spending, incorporating other asset classes like digital gold, and enabling direct savings with brands, reflecting user needs and market opportunities.

Sindhuja sridhar

10 Mar 2021, App Store

The app allows me to make systematic investments towards my financial goals. They have diverse options and the whole process of goal creation is seamless.

The fact that I get rewarded for every goal is an icing on the cake :) The UX is brilliant.

Vishal Kumar

17 Apr 2021, Play Store

Extremely new concept. 👍Super easy to use. Helps people with almost no knowledge in stock to start investing and start saving.���😊

Nilesh Sodhani

3 Jun 2021, Play Store

Great user interface variety of investment options. 1 thing that I liked the most is the #multipl#movement# which says enjoy life, debt free.. And specially thoughts on choosing between impulsive buying or delayed gratification... So no more "Buy Now, Pay Later".

Raghu Chinnannan

21 Sep 2021, Play Store

The concept of rewarding people who has financial discipline and encouraging good savings habit by giving rewards and discounts is great. And the UX is awesome

Bhavik Vachhani

22 Aug 2022, App Store

I came across Multipl approx three months back. It makes goal based investing super easy.

The UI is very easy to use. I would definitely recommend multipl for goal based investing.